Recently, my doctor recommended that I receive a vaccine against whooping cough.

“OK,” I said, my legs dangling off the exam table.

After I agreed, she proceeded to try to sell me on it. Clearly, this doctor was used to being argued with. Although I tend to be a questioner, in this instance, I had no qualms. I’d already done the risk / reward calculation in my head and determined that the reward of avoiding whooping cough outweighed any risk. I also subscribe to the broader philosophy that if you cannot trust recommendations from your doctor, your first order of business is to find a new doctor.

This is not a post in which I wish to argue about choosing doctors or the merits of vaccines. Rather, I wish to posit that considering the risk / reward profile of any action can help you make better and quicker decisions.

I find this frame more useful than creating pros and cons lists. The risk / reward frame puts you in a mindset that implicitly acknowledges this truism: Living involves risk.

There is no such thing as a risk-free existence. Luckily, there’s no such thing as a reward-free existence, either!

Stock investors know this. They are always asking, “What’s my upside? What’s my downside? What’s the risk / reward?” As a stock analyst, I spent a lot of time trying to call bottoms in stocks — meaning, interpreting whether a stock was as low as it could go. Depending on one’s time horizon and risk profile, going long a stock (that is, buying it) when it is at a bottom is not a bad way to grow the portfolio. Minimize risk, maximize reward, make money. (The mindset is easy. Doing it is the hard part.)

You can apply your own internal risk / reward calculation to every major life decision. Even inaction carries risk.

In your personal life, risk tolerance is a spectrum with thrill-seeking dare devils on one end and perhaps accountants on the other. (Calm down. Some of my best friends are accountants.) To the thrill seeker, the reward of the thrill outweighs the risk of death. Put another way, a thrill seeker’s choices are designed to avoid the risk of living a life without exhilaration. Same type of calculation, different tolerance set point.

If you haven’t done so, try putting some upcoming decisions within a risk / reward framework. What’s your absolute downside? What’s the upside? Can you apply probabilities to each — in other words, what are the odds of each happening? Now which side outweighs the other?

We all get this calculation wrong from time to time — that’s called learning.

Non sequitur: Many of our political disagreements are arguments over risk tolerance versus perceived reward. When you disagree with someone, you might try asking yourself how his views play into his perception of risks and rewards and how those might differ from your own. How do probabilities tie in?

Thoughtfulness on a deadline is not a strength I bring to any relationship. In fact, the birthday gift I offer my closest friends is absolving them from having to reciprocate any gifts to me on my birthday.

For some people, gift-giving and anniversary-remembering is a strength. It’s not for others.

Life gets a lot easier when we find what we’re good at and enjoy doing, and do more of that thing. When we play to our strengths, we compound our gains. We end up in relationships, job positions, and careers that are an optimal fit.

Too often, employees and partners spend too much time trying to fix weaknesses. The problem is that one only gets a marginal return on investment when expending energy on a weakness. There’s a reason why it’s a weakness!

This is all personal growth and leadership 101. I’m just adapting it as an excuse to ignore Valentine’s day.

(Note: Many messages sent via this Web site between August 2016 and February 2017 went to my spam folder and I did not see them before they were automatically deleted. Please accept my sincerest apologies, know that it was not personal, and send the message again!)

Starting in September, I started assisting Tesla with investor communications and therefore have been not blogging as much. For one, my days are full. (I am also still doing executive coaching.) For two, it seems fitting to write less.

But I did want to share some thoughts as we head into 2017.

Working at Tesla, you hear the words “first principles” a lot, which has not yet become a widespread business buzzword, but absolutely colors how employees are encouraged to think. Studying Tesla over the years influenced me so much that I named my company, Solve for X Coaching, after this philosophy.

It’s a concept based on physics, which means you take things down to the physics and mathematical levels and question all assumptions. Put another way, you ask “why” continuously until you get down to science (or in my view, in the case of life, guidance from religion or philosophy, and even then, you could probably still drill down deeper to the atomic level.)

It requires that you eliminate thinking by analogy or comparison with known processes. Analogies look at how something else works and then applies that knowledge to the current situation. But the problem with that is that you end up blind to things that could change. Analogies might help in understanding how something works right now, but they don’t help to build something new and better from scratch.

If you apply this way of thinking to the structure of your own life, sometimes dangerous and miraculous things will happen. Dangerous because it’s hard to maintain the status quo if you’ve questioned everything, miraculous because you discover how much of your own life design is within your own power.

It’s hard to do it on one’s own, though, with is why I like being a coach and working with people as they lean forward into their own life designs. We all have blind spots, myself as well. I can’t believe how many huge ones I’ve seen in my own life through executive coaching.

In my own life, when I boil things down to the science, so many of my recent decisions come down to biology and acceptance of that. I have monetary, career, family and motherhood aspirations that often seem to conflict with each other. As a female member of our species with a biologically and psychologically driven desire to reproduce, for instance, I must birth and nurse my offspring and I accept that is a limiting factor on my overall earnings potential. It also defines what I’m solving for now. What I’m solving for in the future will change.

I accept that my two biggest performance constraints in any corporate environment are 1) my biologically and psychologically driven desire to reproduce and care for offspring and 2) my underdeveloped spatial intelligence, in part caused by nearsightedness and astigmatisms, which make me bad at driving and navigating in any environment. Meh. Luckily, I offer enough strengths to compensate for those two.

I share this self-analysis because we can all do something similar in our own lives. It’s hard to be bitter when we own our choices and recognize what is outside of our control. (The rules of science are outside of our control.)

If you are facing conflicting desires or what seems like an unsolvable problem, take it down to first principles, down to the science. Break it all down, nay, wreck it, and build it back up, even if only in your own head. And see what solutions you come up with.

“And so God made the world and stocks and bonds.” —Geoff Dodd, my hilarious and competent Series 7 instructor.

What is Wall Street? What’s the difference between a stock and a bond? Why do we even have a stock market?

You are not alone if you have made it to adulthood and you don’t know these things. I’m going to help you out via an eight-minute read, hopefully in a way that sticks.

A lot of smart people, even with advanced degrees in law or medicine, get fuzzy brained on this stuff.

It’s never formally taught to anyone outside of business, and even people with masters degrees in business need further studying to pass a licensing exam to work in the financial markets.

In fact, much of the media that reports on this stuff doesn’t really understand it. I know because I’ve been a financial journalist and then, as an analyst, have helped journalists at financial publications get up to speed.

You probably know that there is a such thing as a stock market and that you’re supposed to be involved in it to win at life, but maybe then it kind of falls apart for you. And yet, everything about Wall Street is so ubiquitous that nobody is allowed to admit that they don’t know anything about it.

If that last paragraph resonates, then this post is for you. Seriously, no worries.

Here’s a Q&A based on real conversations with friends over the years.

What is Wall Street?

Wall Street is literally a street in the lower Manhattan section of New York city. The New York Stock Exchange is based there.

Wall Street is figuratively a term used to describe the ecosystem of high finance. That includes the broader financial community, hedge funds and mutual funds, brokerages, investment banks, and everything having to do with the capital markets.

In late 2011, when the Occupy Wall Street movement took up space at a lower Manhattan park about two blocks off of the literal Wall Street, a lot of people who work on figurative Wall Street kind of, well, laughed. Because everyone knows the real money is managed out of midtown. And besides, it wasn’t stocks that caused the global financial crisis of 2007-2009. It was bonds. Duh.

What are the capital markets?

A bright and creative English major asked me this once. Great question!

So, capital is a fancy word for money. In general, you wouldn’t use it to describe the cash in your pocket but rather amounts so large that it would be silly to call it “money” anymore, and so we call it “capital.” Capital is synonymous with large sums of wealth or assets.

Capital is fuel for growth. A great idea that would enrich people’s lives at scale would go nowhere without capital.

When someone says, “I need startup capital,” they are referring to the money they need to get their business running — to buy equipment or hire people. When an individual says he hopes to “capitalize” on something, in a literal sense, he means he wants to make money off of it or use it to his advantage in some way. When an investment bank says it wants to capitalize something, it means to fund it, or provide capital for it.

The term capital markets primarily refers to the stock and bond markets.

What are the stock and bond markets?

The best way to answer this question is to first answer the question that you are not asking. Knowing the purpose of a thing can help you to better understand it. Ask me what’s the purpose.

Ok. What is the point of the stock and bond markets?

Yay!

Every business is a glorified lemonade stand. So let’s start there.

Off to a good start. (Photo credit: Rebecca Schley, Flickr, Creative Commons license)

You open your first lemonade stand. It’s popular, people love it. You want to expand. All businesses need money to grow. You calculate that you’ll need $70,000 to open a physical store on Main Street.

To generate this $70,000, you could use your own money. But maybe you don’t have $70,000 laying around (because if you did you might be smarter than going into the lemonade business?) Anyway, to raise the money, you could go to a local retail bank* or credit union.

Ok, so you go to the bank and the friendly loan officer gives you a bank loan and you use it to open your lemonade stand.

Now let’s say your lemonade stand is awesome and you decide to expand nationwide. What do you do next**?

If you need a tens of millions of dollars, you might raise what’s called venture capital. Venture capital, or VC money, comes from wealthy people called venture capitalists who run their own companies, aka VC firms, that take big risks on startups in hopes of making more money later.

But what if you wanted to raise hundreds of millions of dollars?

Well, then you would turn to the capital markets: Wall Street.

Organizing funding so that companies can grow is exactly what Wall Street is for***.

If you need hundreds of millions of dollars to make your dream a reality, no retail bank is going to lend it to you. To raise large sums, you need an investment bank, the ten largest of which are JPMorgan Chase, Goldman Sachs, Bank of America Merrill Lynch, Morgan Stanley, Citigroup, Deutsche Bank, Credit Suisse, Barclays, UBS and Wells Fargo.

In sum, there are two primary ways to raise a lot of money:

If you sell stocks, then you are selling equity. Another way to say this is that you are raising equity, that is, selling shares of ownership of your company. Others buy a little piece of your company, or a share of your company, and you get the shareholders’ money. In return, you no longer own 100% of your business. When a corporation sells stock to the public for the first time, that is known as an initial public offering, or IPO.

What is cool about raising money by selling stock in your company is that you never have to pay that money back. What sucks is that your profit forevermore belongs to the shareholders in proportion to their ownership percentage. The only way to get back ownership is to buy back your own stock. Once you sell equity, it is sold, no matter how big your company gets.

In sum: Stocks are equity and equity means ownership. The holder of the stock is an owner of the company.

If you sell bonds, then you are selling debt. In other words, you are borrowing money that you eventually have to pay back with interest. On the other hand, the ownership structure is maintained. After bond holders are paid back with interest, they have no claim on the company. Your company could grow to the moon and all that profit is yours so long as you own 100%.

In sum: Bonds are borrowing and borrowing means debt. The holder of the bond is a lender to the company.

That’s the point of view of the company that needs capital.

On the flip side of all that is the investor — the person who lends or gives money to the company that needs it. If you’re reading this blog, you are probably an investor in some form. Investors are anyone with an individual retirement account, anyone counting on a pension, anyone who puts money into a 401(k), and all the people on up the money management chain who guide an individual’s money into a proper portfolio of investments.

Wall Street’s basic function is to allow money to flow to where it is most needed. This flow makes modern life possible.

In the case of bonds, entities borrow from future earnings to make that future better in some way. In the case of stocks, entities democratize their future earnings by allowing people to take a risk and invest, and hopefully gain wealth without expending effort.

Ok, so the point is to get money from the people who want to invest and give it to the people who need it. I still don’t get the New York Stock Exchange. What are the stock and bond markets?

Ok so let’s say Jill buys shares in Tom’s lemonade stand company. Jill buys $2,000 worth of stock in Tom’s company. Tom got his money, good for him. Jill now gets a share of Tom’s profits, no matter how small. Is Jill stuck with that investment for life? No. Jill can turn around and sell her shares to someone else. But she needs a market to do that.

After a corporation (or government entity) has raised money by selling stocks or bonds, the stock holders and bond holders can sell their holdings to other people. This is called trading**** and it happens in what’s known as the secondary market.

When you think of the stock market, you are thinking about the secondary market, which is the trading, or buying and selling, of shares of corporations. The initial purpose of raising money for the company has been met, and now the shares trade. The value at which shares trade depends on how buyers and sellers view that company’s future prospects. By value, I mean stock price.

As opposed to bonds, stocks are the easiest to understand and the easiest for media to report on. That’s because the stock exchanges are highly regulated and public. Some of the largest are the New York Stock Exchange (NYSE), the NASDAQ, the London Stock Exchange Group (LSE), and the Japan Exchange Group (JPX). The stock markets have a definite opening time each morning, a closing time, and an after-markets trading time.

Stocks are cool because you can know a given stock price at any time. Tesla shares closed at $222.93 today, which Google told me, here.

The stock market is bold, beautiful and open. There’s glamour to it. The media loves it. Many people understand it.

The bond market is more, uh, dark. And confusing. And it’s way way way bigger than the equity market. Remember the subprime lending crisis that caused the Great Recession of 2007-2009? Yeah, that happened in the bond market.

The mainstream press rarely writes about the bond market. It’s a snoozer of a topic, the prices aren’t public, and bonds are way confusing.

If you want to check the price of a bond, you have to call your broker. And he’d find out the price by calling someone else. I think. And check his Bloomberg screen. Or something.

If you specialize in debt structures or bonds in this lifetime, you can make a killing.

Is there anything else I should know?

There’s a lot more to all this, but you now know enough to make people avoid you at parties.

Know that the word security refers to any type of financial instrument, including stocks, bonds, some types of insurance, and options. And that there are lots of different types of securities to invest in — basically products created by the financial world.

Also, know that I used the term bonds loosely here and that other debt instruments include notes and bills.

Finally, I used corporations as an example here. Know that beyond corporations, governments are huge participants in the debt markets. As of this writing, the US government has $19,443,266,164,413.41 in debt outstanding. In English, that’s nineteen trillion, four-hundred-and-forty-three billion, two-hundred-and-sixty-six-million, one-hundred-and-sixty-four thousand, four hundred and thirteen dollars and forty one cents. All of that debt is held by individuals, institutions and other governments in the form of bonds, notes and bills.

Commodities are super fun and also have markets. Commodities include hogs, corn, currencies, wheat, oil, rice and so on. I’ve toured the Chicago Board of Trade in Chicago where everything is traded from corn to hogs to cattle, done in trading pits of men yelling at each other. Incredible to watch.

Footnotes:

*You could also do a Kickstarter or open a GoFundMe account to collect from people. I believe that it’s a bit disingenuous to ask other people to fund your dream without giving those people a return, but there’s a market for it and it seems to work for some. Here’s my unofficial simplified hierarchy of raising capital, by amount needed:

family and friends

kickstarter / crowd funding

community / retail / commercial bank loan

venture capital series A round

venture capital series B round

venture capital series C-F round

private equity raise

Initial Public Offering (IPO) / Debt offering

Secondary offering / Debt offering / Convert / Line of Credit, etc.

***In May 2015, I wrote to investor clients a partially tongue-in-cheek e-mail about concerns about Tesla’s cash burn. My e-mail was later quoted by Bloomberg News. Notice how much Wall Street looks at cash, capital, and access to capital. Excerpt from my e-mail:

I saw some hand-wringing this morning in other’s published research about Tesla’s cash burn. I think this is missing the point – the current cash burn rate is not a solid-set-in-stone line. Tesla has the option of drawing down further on its warehouse line and opening new lines to recoup the cash off of its leased vehicles. Also, deliveries in Q4 will be roughly 2x what they were in Q1, whereas expenses will only grow ~15% in that amount of time. And, in Q1, Tesla’s SG&A (recurring cash burn) actually ticked down sequentially, so they are to be commended for that – good cost control in Q1.

Finally, it turns out that Wall Street has some great solutions for companies in need of capital. In fact, funding rapid growth and sea change through companies such as Tesla is exactly what Wall Street is for. Worst case, a straight-up equity raise (and Tesla likely has even more favorable options) at the current level would raise more than $1b with about 3% dilution. As far as bear arguments go, the cash burn one misses the mark.

****I have yet to meet a stock trader I didn’t like. Traders are the blue collar Wall Street folks — usually pretty colorful and inappropriate. They’re forced to live in the moment as they enact trades and try to get the best price for clients. It’s almost like playing a sport.

Let’s take a second to analyze the division of labor within a family unit.

There are three main jobs when it comes to running house and home with kids.

Sales: Full-time work that pays the bills and brings in income for necessities, including food, healthcare and shelter. Basically, this is like the “sales” function as it is the outward facing function that brings in the revenue.

Operations: Full time child care includes watching and caring for the children, managing their education and their welfare. This is the primary caregiver function, a combination of human resources and operations.

Back office: Home maintenance, bill paying, grocery shopping, and house keeping. This includes janitorial work, some operations-type activities, and back office administration.

I’ve always been a working mom, since my newborn was five days old. And in doing so, I’ve analyzed the family unit and this is my conclusion:

The stay-at-home parents of young children do not have time to clean the house properly. They’re too busy taking care of the kids.

I know this because I have always outsourced week day child care to au pairs. It’s my job to manage the child care and decide what to outsource. Here is what I have outsourced to au pairs during my work hours:

administering to the child’s every need

dressing the child, doing her hair

entertaining the child

preventing the child from destroying our house

making sure the child does not kill or gravely injure herself

washing the child’s laundry

neatening up the child’s room

preparing two healthy meals per day for the child and cleaning up after those meals

taking the child to the park, playground, zoo, aquarium, public library, and museums

(censored: bathroom related)

reading to the child

The au pair also helps keeps the kitchen neat, as we all do, and must find time in that 9-hour workday to feed herself.

Nowhere in that full-time work schedule is there time to vacuum underneath the sofa, mop the floors, toothbrush the grout, or scrub the toilets. And yet, I have stay-at-home-mom friends who do all that plus all the cleaning.

Somewhere along the line, child care and housework became synonymous and inseparable. They are not.

If you’re a family with children, presumably part of your raison d’être is the successful raising of children. So if you’re the working parent expecting the stay at home parent to do all of the cleaning, consider this: Just as Google doesn’t task its engineers with janitorial duties, the stay at home parent’s primary task is not cleaning. Similarly, with factory work, the workers who operate the machines or make the widgets are not the same as the ones who clean.

In sum, housework is a third task and it is separate from child care.

You either have to outsource this third and part-time task — I highly recommend giving up something else in some other area of life to do this — or come up with a separate plan for how both parents* will split that duty.

The house work plan — insourced or outsourced — is separate from the child care plan.

(*This analogy is a two-parent family unit analogy, with apologies to the single parents out there slaying it every day and handling the sales, operations and human resources functions all on their own. Hats off to you.)

Something fascinating is going on with negative interest rate policy: It’s having the opposite of its intended effect.

A negative interest rate is a simple concept — it means that money in a bank account shrinks over time, rather than grows. It takes the time value of money and heightens it by penalizing saving.

The concept started in 2014 in Europe and since, Japan has also followed suit. Negative interest rates are applied to reserves held by commercial banks, meaning that no small time individual is going to lose the nominal value of the money in his bank account. The policy trickles out to create negative yields on government bonds — meaning that if you put 100 units of currency into a bond, you won’t get all 100 back at maturity — and onto large institutional savers — meaning that entities with large sums of money sometimes have to pay the bank to store their money.

The US does not have negative interest rates, but because other countries do, the US has to hold interest rates low to keep the dollar competitive. (A strong local currency is not always a good thing because it makes your exports more expensive.) See the chart below? If you know what you’re looking at, that interest rate chart tells you nearly everything you need to know about access to wealth, success, income inequality, and the post-Great Recession economic recovery.

How does this affect you? Well, it means that you aren’t going to get a lot of return on your savings account any time soon. It means that home values are going to continue to rise quickly in economic hot beds, as access to capital remains cheap. And, in theory, it should make you want to invest your money in stocks, in new business ventures, or in consumption of goods.

But, does it?

Low interest rates seem to have worked. But negative interest rates are still untested.

The purpose of negative interest rates is to encourage financial activity, lending, and inflation. A negative interest rate is a “use it or lose it” policy — it encourages commercial banks to lend money rather than to save it. It is supposed to create a mentality similar to your “use it or lose it” vacation leave or flex account — when you know that your asset is going to be lost over time, you’re encouraged to use it now. And this mentality is meant to trickle out to consumers.

But here’s the problem: Negative interest rates are bad psychology. It communicates uncertainty and thus, encourages individuals to act cautiously and to save more money. Instead of creating a free-for-all of money flow, people are hunkering down, spending less, and saving more.

The Wall Street Journal today quotes several people who are hunkering down and cites statistics on reduced consumption after negative interest rate policies were implemented. People are feeling that they need to save more today to build up wealth. (Not mentioned: I guess these folks don’t want to take their chances with the stock market.)

The interest rate on three-month US treasuries. (Source: barchart.com)

And this makes perfect psychological sense. We know that when people feel richer, they are more likely to spend on consumption, more likely to take risks. Negative interest rates are meant to communicate that it is riskier to leave your money in savings than to spend or invest it now — that’s the rational outcome.

But that’s not how people think. People are not perfectly rational with their money. Individuals are certainly not trained to consider inflation risk.

I wonder if the problem is not so much with negative interest rate policy as it is with how it’s communicated. Because here’s what it means to the financially enlightened: It is still probably a good time to take risks or to start a business. The US is not likely to grow interest rates while trading partners are stuck at negative.

Here is also what it says to me: The ‘experts’ are acting on theory, trying their best, but never really fully sure of what they’re doing and not good at measuring unintended consequences. Economic policy is experimental.

Some time a bit ago, a Seattle pastor posted this challenge question to Facebook: “To whom will you bring comfort today?”

It was early morning on the West Coast, which meant I had been working about five hours already. I thought back over my morning spent with clients discussing a stock that was selling off that day. My clients and I commiserated. We looked at what we got wrong. We looked to see if we could offset at least some of the blame to the management team. Some clients ranted and raged. Some were quiet and steady. All needed a confidential and trusted place to go over their thinking and decide what to do next.

What do you do when things go horribly wrong? When the amount of money being lost has more zeros than the average person can fathom?

You process it, you manage the cortisol pulsing through your blood stream to get to a place of rational thought, and ultimately, you have to decide on what to do next: Sell the position or double down at this lower level?

To whom was I bringing comfort? Hedge fund managers.

My position was a privileged one. For seven years, I studied the intersection of fear, greed and anxiety through thousands of conversations with extremely bright people. It was all very human and very fascinating.

Sometimes, we had the craziest high-five thrills I’d ever experienced. “Love that money! Woo!” – Ricky Bobby, Talladega Nights

Other times, it was vomit-inducing stressful.

Welcome to Wall Street.

If you manage assets* for a living, then I want you to know that part of the reason why your job makes you so anxious is because it is supposed to. People pay other people to manage their money for them as way to outsource financial anxiety.

People on Wall Street are paid to worry.

There are few industries where constantly anticipating what could go wrong is not the result of paranoia, but is actually part of the job description. (Military and tactical law enforcement are others.) The mental health profession says hyper-vigilance is a symptom of PTSD. On Wall Street, it’s a symptom of a job well done.

What’s that? It’s Thursday and you haven’t seen your kids since Sunday night, you’re fantasizing about moving away to a Greek island (or Florida), you have a vacation planned that will probably get eaten away by unforeseen events, and you find yourself taking your first deep breath of the day after market close?

No, you’re not crazy or doing it wrong. That’s your job.

Now go check your bank account. Ahh. Isn’t that better?

Also fun: Failure is never an option.

There is one way to be right: Beat the market.

There are infinite ways to be wrong.

Do you know what science calls it when there are infinite ways to have disorder and one way to have order? Entropy.

“Your job as an investor is nearly impossible: to make great decisions with incomplete information, while reducing uncertainty,” says Marc Balcer, a former hedge fund founder who now runs his own mindfulness coaching practice. He coaches people on how to manage high stress situations. Like me, he works with many Wall Street clients.

I’d like to share some observations that I believe affect the entire economy — from how publicly traded companies manage their businesses on a quarterly basis, to how capital is allocated, to the risk tolerance of ourselves, as a society.

And here, I’m just talking about stocks. I’m ignoring the gigantic, can’t be overstated how big, world of bond investing.

Investors – and people like me on the sell side who served them — are expected to predict future events and predict how a stock will react to those events.

Every quarterly earnings season is go-time in the world of stock investing. Do or die, the final accounting of our predictions in the quarter. Companies report out their financial performance and asset managers score themselves on their bets and then report out to their own clients on how the fund is performing.

Earnings season is The Reckoning. A typical portfolio of 12 stocks is going to have 48 reckonings per year. Plus, all the peers will report and those also move the market — and maybe the fund should have invested with one of them, instead. During earnings season, free time disappears and decision making rules the day.

Everyone is on high alert. Everyone is stressed. Decision fatigue becomes a real thing. It’s tough to manage constant reckonings. Everyone is constantly scored on the manifestations of their hard work, and performance is critiqued by colleagues, competitors, and clients.

Generally, the faster the money moves in a fund, the more stressed everyone is. The hierarchy of stress starts with the long-term mutual fund managers at the bottom (still paying attention but not as frantic) and increases until you get the fast money long-short funds at the top of the stress heap (huge amount of pressure to change positions rapidly and make decisions in the face of incomplete information.)

I knew of several portfolio managers who were red-faced screamers. I worked with them as well as the analysts who reported to them. In every case, it was a fast money fund and the portfolio manager, though behaving horribly, in my view had a lot of public face on the line: In every case, he was managing the assets of people in his own social group. It’s one thing to lose your own money. It’s quite another to lose all your friends’ money.

(And while I think there is never a good excuse for treating someone wrong, I know during the most intense periods, I was not always the kindest -ahem- to my own junior analysts. Reputation, ego, perfectionism, winnersville versus losersville, tight deadlines, seconds mattering — it all played a role. I was not above completely losing my shit over a misplaced decimal point in a financial model. And unlike the buy side, I never actually had any money on the line.)

Here are some sample ways to be wrong:

Be sort of right and sort of wrong = Wrong.

Be right on what happened, but wrong on how the stock reacted = Wrong.

Be right on how the stock would react, but too early on the timing = Wrong.

Be right on how the stock would react, but failed to convince the portfolio manager to adjust the position = Wrong.

Be totally right on the events that would happen and how the stock would react, fail to trim the position and lock in the gain, the next day something crazy happens and the gains are wiped out = Wrong.

Be totally right on the events that would happen, trim the position to lock in the gain, the next day it gets even better and the stock’s up another 15 points = Wrong.

Freak out and sell the position when its down 20 points, and it moves upward another 15 the next day = Wrong.

Be completely right but lose the trust of the PM and nobody acts on your recommendation = Wrong.

Be right but fail to pound the table hard enough = Wrong.

Learn from that mistake, next time make a high conviction call and pound hard, and this time, get it wrong = Wrong.

Have a great year but still under-perform the general market = Wrong.

Be right on nearly minute detail but fail to anticipate that demand for copper in China is going to compress the gross margins of this US industrial by 2 points, causing the company to miss EPS by $0.01 when the Street was expecting a beat and raise = Wrong.

You see? Infinite ways to be wrong. Entropy.

It’s never dull. It’s all-consuming. People use all of their energy to not go nuts. And everyone is dropping fucks like dollar bills

Most hedge fund employees I know — from the folks at the top to the n00bie analysts — take the job seriously. They want to do the best job they can, make a good living, and go home and kiss their kids at night. (Or, if they’re single, party.) They love the money (who wouldn’t?), appreciate the meritocracy, crave the intellectual stimulation, and treasure having some power. There are cheaters and losers as in any industry. I never met anyone shifty or dishonest — that’s my honest truth.

The deeper I get into being a coach for executives and high-performing professionals, the more I learn about the importance of being calm and differentiated — of knowing where one person stops and where another begins, and of the importance of a confidential and trusted space to think. I realize that in many ways, it is what I’ve been doing all along.

You’ll never eliminate anxiety — you’re paid to be anxious.

But, you can manage your anxiety and with enough self care and awareness, channel that energy into making better investment decisions.

**HUGS**

—–

*For non Wall Streeters reading this blog, asset management refers to the profession around managing money. That money is managed in sums so large that it’s not even called money any more, but rather, assets, or capital. Thus, when we say the capital markets, we generally mean the stock market and the bond markets, where large sums of capital change hands every day.

If your retirement account is held in a managed fund, then there’s someone on Wall Street managing your money — either working for a mutual fund, a pension fund, or a hedge fund. And, since many pension funds outsource some asset management to hedge funds, there’s a chance that your retirement account is influenced by the hedge fund community.

The PM acronym is for portfolio manager, the person who has the job of making buy or sell decisions, and the one who usually bears the brunt of the credit, blame, and stress.

One thing I am loving about coaching is that I get to enter into someone’s life or business as a co-mind on decision points. Coaching helps people not only make better decisions, but also identify when a decision needs to be made, or doesn’t.

A key question to ask yourself about a certain action is: Am I doing this as a result of a conscious decision? Or is the action the result of unconscious inertia?

Unconscious inertia is when your actions are the result of not questioning the status quo, or the decision process gets stuck just below the surface of active thinking and awareness.

Four random examples:

1.) A small firm has grown to the point where it could justify hiring another employee to share the workload. Hiring the employee would bring more breathing room into the schedules of the principal or owners. However, hiring the employee is risky. What if business trends down? Nobody wants to have to lay someone off. And so, nothing is done.

But there’s a decision point in there. Maybe, the risk of hiring an employee is too great and you make the decision not to proceed. That’s OK. Or maybe, after some more financial analysis on risk/reward, you feel confident opening the position and seeking the right hire. If I were coaching such a scenario, I’d also gently point out that interviewing candidates is still not hiring them, it’s just exploring a potential future reality and seeing how it sits with you.

2.) A couple has lived together for seven years — ever since graduating college. They are approaching age 30 and have not married. Days pass and no decision is made. Is it possible to make a decision that takes unconscious inertia and replaces it with decided action? Especially with something as big and sometimes scary as committing to a life partner, you can use smaller decisions to lead to bigger decisions. Maybe you even decide to not decide until a future date. What good does that do? It forces conscious thinking into your actions.

3.) One of my favorite decisions is choosing to invest in a sabbatical, a period of time to honor one’s life transition and figure out one’s next step. Isn’t that a beautiful decision? You’re not picking your next step, you’re deciding to give yourself time to decide. Then, your days are considered and active. (Plug: A sabbatical is a great time to invest in yourself with a professional coach.)

4.) You invested in a stock and it’s moved in a particular direction, or has done nothing at all. Do you buy, sell, or hold? Buying or selling are obviously the result of a conscious decision. “Holding” should be, too. (…Gosh, I love the lessons of the stock market — are they not applicable to life, or what?)

So long as you’re not causing undue pain to others, there is probably no right or wrong decision.

Just don’t let unconscious inertia decide for you.

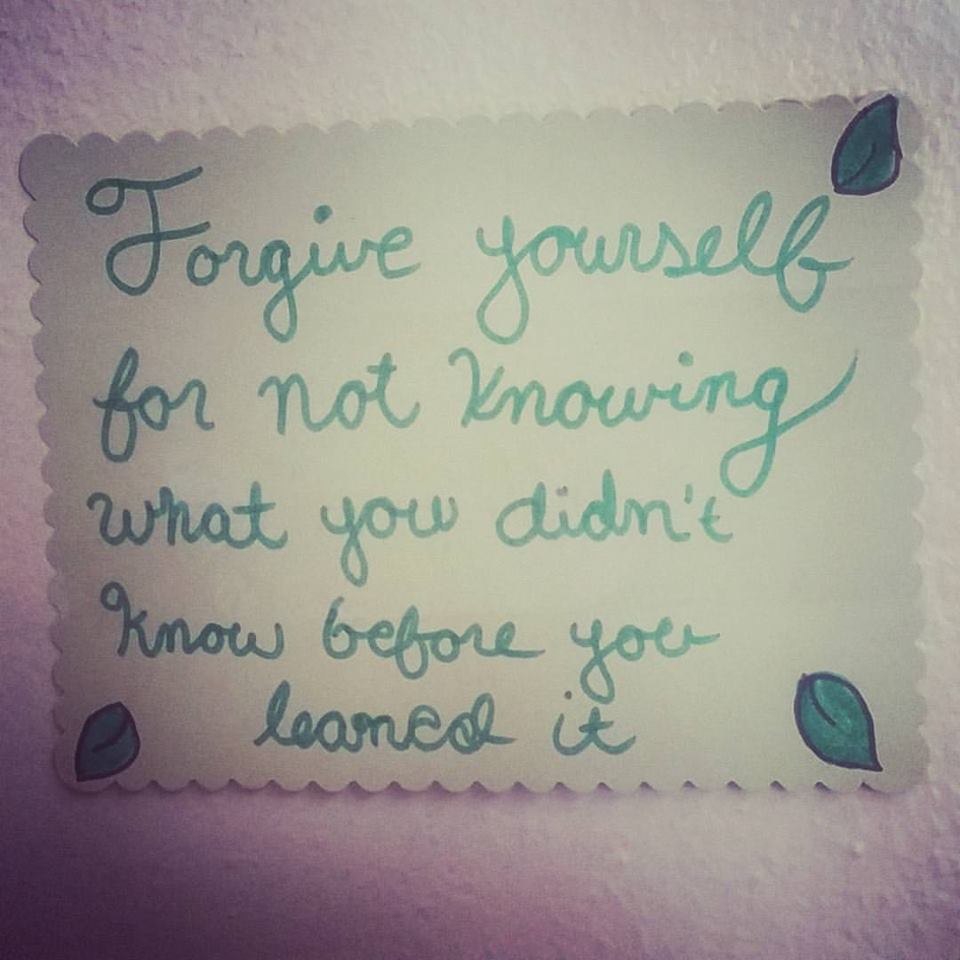

“Forgive yourself for not knowing what you didn’t know before you learned it.”

True of stock investing. True of life, too.

We are all beginners. There is never a time in life when we are not beginners at something.

(Aside: I pledged earlier this week to teach myself SnapChat. God help me!)

Life is giving us an education. We are paying for that education and so are the people we make mistakes on. Yikes. But there is no other way.

These two stories helped give me perspective over the years:

One. President George Washington was a successful Revolutionary War commander and most of us know his success story. But, he made many mistakes as a young man in the French and Indian War. Washington’s men paid for his military education with their lives.

Two. The famous book, “Man’s Search for Meaning,” is written by Viktor Frankl, an Austrian psychiatrist who survived the holocaust and three years in the camps, including Auschwitz. His odds of survival were grim — he was most likely to be killed right away, or worked until the last ounce of his energy had been spent, at which point he’d die of starvation, sickness, or a Nazi guard’s beating. He describes how every decision the prisoner made was a life or death choice. Should one choose this queue or that? He had mere seconds to decide with an incomplete information set. He could march in the direction of a prisoner work hut where he would live, or the gas chamber, where he would die. The lines were not marked. Luck and chance played a role. He could line up in a work group where the guards were in a bad mood and would later shoot him for no reason, or he’d line up with a more merciful guard who might slip a candy bar when no one was looking. These poor souls in the camps were forced to make fateful decisions without being able to see the future or the big picture.

So, too, are we all making decisions with the best set of data we have. Only, if you’re reading this blog, the consequences for you won’t be nearly so dire, and what a relief.

Tesla Motors reports its quarterly earnings this evening, and for the first time in 21 quarters, I will not be on the call asking Elon Musk & crew a question.

As of May 2016, I am stepping back from day to day coverage of Tesla Motors. I’ll remain affiliated with my firm as an advisory analyst and will be working behind the scenes with my analyst replacement.

Here’s why.

My office has a sloping ceiling, and on the slant just within my gaze are large stenciled numbers: 2061. That is the year that my life expectancy runs out, based on a typical aged 34 female. I rarely share this fact because it sounds a bit disturbing and morbid.

But for me, it provides focus.

I work better with a deadline.

And I feel strongly that my work as a stock analyst is done and it is time for me to move on to other things.

I am launching my own executive / professional coaching business, Solve for X Coaching, where I will work with executives and mid-career professionals on life transition and communication & leadership style.

Being a Wall Street stock analyst on Tesla Motors (TSLA) shares from 2010 to 2016 has greatly enriched my life and understanding of the world. I took pride in the depth of my analysis and research — I always started from a position of skepticism and asking, “Where could Tesla go wrong?” But early on, it became clear that the bigger question — the world changing one — was, “Where could Tesla go right?”

My firm gave me the opportunity to call the truth on Tesla as I see it. And we get to that truth by analyzing the following three questions, at their simplest: Does Tesla have a technology lead that is real? Can Tesla build it? Will people come?

Answering those questions took me on a journey into researching battery pack manufacturing, touring battery manufacturing competitors, creating relationships with suppliers, and constantly talking with industry. My financial model, which I built from scratch, modeled out Tesla revenue and expenses for the next several years at a granular level — even at some points analyzing the costs of a lithium-ion battery down to the cathode, anode, electrolyte and separator. I have written volumes of research for Wall Street clients addressing Tesla-related topics. Unfortunately, that research is not available to the general public and was shared only with firm clients.

Does Tesla have a technology lead that is real? Can Tesla build it? Will people come?

Yes, yes and yes.

The quarterly earnings conference calls were just a small part of my research on Tesla, but they were usually fun and productive. I have helped to generate some informative conversations with CEO Elon Musk, CTO JB Straubel and the rest of the Tesla team over the years — my questions have unearthed the Gigafactory plans, whether Tesla really needs to produce the Model X, and whether, given constraints, Tesla would build batteries for electric cars or solar storage. I’ll truly miss that part of the job.

As an independent third-party analyst, I’ve always been prohibited from personally buying the stock. I can’t wait to buy in.